Boomer or Bust, by Irina Ratsek, YS Magazine

There’s only so much time to be born, live, learn, find a career, save up, and retire. The differences between the generations couldn’t be more stark. It is, quite frankly, getting harder out there. As the economy continues expanding into high technology, information economies, and Wall Street schemes, and away from manufacturing jobs and corporate responsibility, retirement has never been so grim a prospect. Do you have a plan?

Some retirees are feeling comfortable with hefty retirement funds, while many retirees (current and soon-to-be) are facing the prospect of working into late life or foregoing retirement altogether. Retirees then face the task of dispossessing themselves of the personal wealth in the form of charitable giving and bequeathments. What will happen to the money retirees leave behind? Will Boomers leave behind large sums of money to their children or become philanthropists in their final years?

Local CU Boulder Professor and DeMuth Chair of Business Law, Peter H. Huang, studies retirement. In his Stanford Journal of Business and Law article, Achieving American Retirement Prosperity by Changing Americans’ Thinking About Retirement (2017), he says, “As a society, we should not expect most Americans will plan well for their retirement left on their own because doing so entails a non-trivial set of difficult cognitive tasks and it is unclear who is a trustworthy advisor.” Complications of retirement planning, coupled with threats to retirement, an uneasy job market, and a bleak outlook makes planning for the future increasingly daunting.

Stock photo

The Generations

The two major groups facing the American retirement crisis are Baby Boomers and Generation X. Millennials are a third concern, but having entered the workforce at a younger age and thus being younger during our most recent Great Recession, the majority have already recovered. “One in five are very confident that they will be able to live a comfortable lifestyle in retirement. 60 percent expect to retire before age 65.” One in five is not an optimistic statistic, but having started to save at the median age of 22, on average, and living frugally those who have heeded the lessons and prepared should be relatively comfortable.

The less-than-rosy self reporting may also be based on other factors, including a continued sluggish economy and the lack of movement to address major issues both nationwide and in Washington D.C., the political class, notably on the right, sitting on their hands as America continues exporting jobs, rewarding the 1 percent for work by the rest, and ignoring the nearly irreversible, spiraling death of our planet.

Many Boomers (born 1946-1964) from the front half of their generation have already retired, while the tail end of Boomers are almost universally still working. The last of the Boomers won’t turn 65 till 2029 and, with a lifestyle and health outlook greater than their parent’s generation, we can expect them to wield serious influence over the direction of the economy over the next generation and a half (almost 30 years). By 2030, adults 65 and over are expected to comprise 20 percent of the population here in Boulder County (Boulder County Trends 2013). Overall, that means that there will still be over 61 million Boomers—about 17.2 percent of the projected US population, witih high influence over the economy in 2029, whether they hoarde or give away their money (Colby, Sandra L, et al. 2014).

Boomers represent the major slice of the economic pie. Despite overall generational wealth, many are facing an uncertain retirement, with nearly two-thirds planning to work into late age and beyond, according to USA Today, while only 60 percent of baby boomers report having any retirement savings at all, and near 40 percent reporting under $50,000. “Almost one in three Americans age 65 to 69 is still working, along with almost one in five in their early 70s,” according to Bloomberg. Working into late life will become more common for those who struggle to save. In actuality, we can expect to see many Boomers increase wealth as their parents, the Silent Generation, aged 70-87 in 2015, leave their own fortunes behind, though that money won’t be spread out evenly across the generation.

Generation X (born 1965-1978) began working in the 1980s and was the first “to have access to 401(k) plans for most of their working careers. They started saving for retirement at a median age of 27.” They’re feeling pretty good about their retirement outlooks, with the majority planning to self-fund their retirement. The problem is, most are under saving for retirement, with only about $70,000 of the expected $1,000,000 parachute required for a soft retirement landing. “Generation X will begin turning 50 next year, a loud wake-up call for them to get laser focused on planning, saving and investing for retirement. Their clock is ticking but they still have time…” said Catherine Collinson, president of the Transamerica Center for Retirement Studies. In fact, their 2016 study found “that baby boomers […] have median retirement savings of $147,000. A typical member of Generation X […] has socked away $69,000. Meanwhile, the youngest generation in the workforce, Millennials […] have a median retirement savings of $31,000.”

This Generation X outlook works with wealth management predictions, as increasing “incomes and savings [in later life] will help them amass a net worth of $37 trillion in 2030,” just behind Boomers, but taking over the lion’s share of net wealth shortly thereafter. Boomers retiring and beginning to pass will fuel Generation X wealth accumulations as much as incomes and savings, though, and it’s important to pay attention to bequeathments received by Boomers, as they will pass that money along, as a primary indicator of generational wealth building over the next 30 years.

The Great Post-Ought Transfer

The fact is, according to an aptly named article from Bloomberg, Americans Are Retiring Later, Dying Sooner and Sicker In-Between, Americans are retiring later—note the increase in retirement age to 67 from 65 by 2027—without a parallel increase in life expectancy. Data suggest, “Americans’ health is declining and millions of middle-age workers face the prospect of shorter, and less active, retirements than their parents enjoyed.” This is important in discussions of bequeathments because Boomers will transfer wealth to following generations quicker than the Silent Generation is transferring to them. Why? As noted, the Boomers are facing shorter life spans (as are Generation X), meaning they’ll pass on wealth quicker.

Deloitte, a wealth management companies, is already speculating on the age distribution of bequests as first the Silent Generation and then Boomers begin to settle account and prepare final wills. In a recent article, The future of wealth in the United States: Mapping trends in generational wealth, Deloitte is clear on advice to money managers that, “for financial firms to fully exploit these potential opportunities, they will need a refined understanding of how this wealth will be distributed among different age cohorts.”

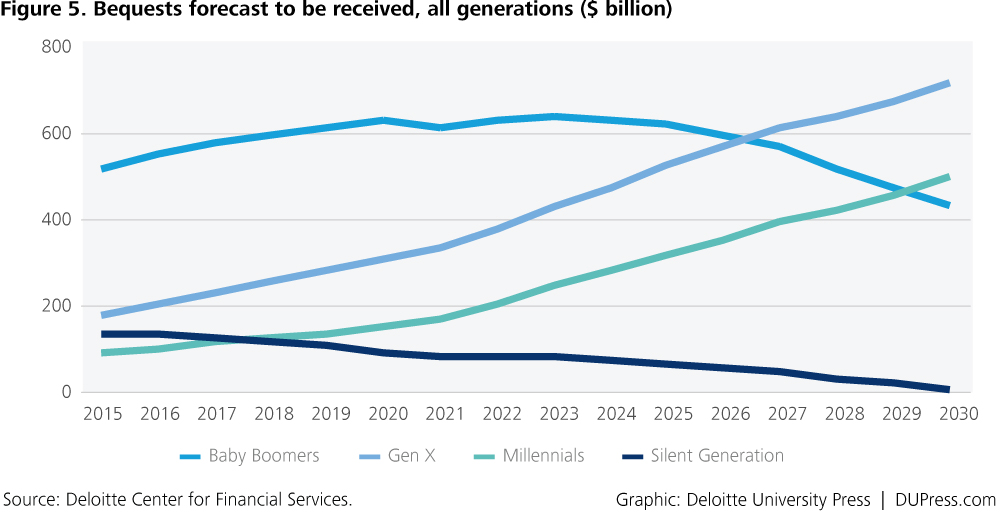

Screenshot, Deloitte Bequests projection

It’s important, when looking at projections from Deloitte or any other money management firm, to be cautious of the logics employed. They paint a rosy picture based on data compiled over decades of inflation, often without correcting for that inflation moving forward. “Investors who rely on historical returns for the past 50 years will ‘probably overestimate what we’re likely to see in the future,’ says Chris Jones, chief investment officer for Financial Engines, a retirement-plan consultant. In the same piece, Greg Womack of Womack Investment Advisers in Edmond, OK., says “overly rosy projections represent one of the biggest pitfalls in retirement planning.”

The Deloitte Center for Financial Services expects US household assets to increase from about $72 trillion in 2015 to $120 trillion by 2030 (the year after the last Boomers have reached retirement age). Boomers currently hold about 50 percent of household wealth with their parents, the Silent Generation, still holding about 30 percent. Boomers are projected to remain the wealthiest generation until at least 2030, after which “their share of net household wealth will peak at 50.2 percent by 2020 and decline to 44.5 percent by 2030,” as older Boomers begin to pass.

That is, “Boomers’ financial assets will peak at nearly $26 trillion in 2029, rising from over $17 trillion in 2015.” Offering a rosier outlook for Boomers, US News and World Report says that by 2029, “controlling 70 percent of all disposable income in the United States, Boomers [will continue to be] a dominant financial force in the marketplace,” peaking at $53 trillion.

In comparison, “Generation X will experience the highest increase in share of national wealth, growing from under 14 percent in 2015 to nearly 31 percent by 2030; from $35 trillion in 2015 to nearly $64 trillion by 2030. Millennials will experience the fastest growth rate of net wealth, however, Millennial share of national household wealth will remain below 20 percent, in line with Millenial’s early savings and pessimistic outlook. Millennials’ do, however, stand to “benefit from potential increases in labor force participation rate, as well as from increasing salaries as older Millennials are promoted to higher-paying jobs. Millennials’ assets are projected to grow from $1.4 trillion in 2015 to $11.3 trillion in 2030.”

While much of the increase in wealth is predicated on growth of retirement savings accounts, increased savings by Generation X and Millennials, and overall economic growth, there is a huge transfer of personal household wealth expected in the form of bequests and philanthropy. Deloitte points out that, “over the next 15 years, nearly $24 trillion will be transferred in bequests (after taxes and charitable giving), reflecting spousal, inter-, and intra-generational wealth transfers.” From their research methodology, charitable giving is estimated at 10 percent of holdings.

That is, “the Silent Generation, whose youngest members are 70 years old, still commands nearly $24 trillion in wealth,” in spite of the fact that members began passing decades ago. A critical reason the Silent Generation still commands such a staggering amount of wealth is because, “large number of Silent Generation members—29 million as of 2014—are still alive.”

As the Silent Generation passes, will they bequeath all their holdings to their children (Boomers), or will their grandkids (Generation X) get a slice? Much of the intergenerational wealth held will be transferred into Boomer pockets, though there is no way to predict how much will go directly to Boomers instead of being spread out. Keeping in mind that much of the Silent Generation’s wealth is held among a relatively small percent of their population, and thus a larger share of boomers will receive very little (if anything), their wealth will secure retirements for many Boomers, enabling them to decide how they spend retirements and what they spend on during retirement. Boomer bequests received were over $500 billion in 2015 alone, and are expected to peak in 2023 at just over $600 billion, as that $24 trillion is passed on from the accounts of those who have passed on. Generation X will take over at the head of the bequests received line around 2026, passing the $700 billion mark around 2030. Of course, that’s just a projection. Where exactly will Boomer bucks go at end of life?

Stock photo

Where Nest Eggs are Going

Over the next 20 years, Boomers are expected to donate $6 trillion directly with an additional $1 trillion donated in the form of volunteer services, according to a report by Age Wave in partnership with Merrill Lynch Global Wealth Management. The report finds, “baby boomers are 49 percent more likely than their parents to make an effort to find out how nonprofits use their money before they decide to donate, and 44 percent of them want to direct how their charitable gifts are used, compared with only 15 percent of their parents’ generation.” Boomers aren’t planning to sit on their wealth the way the Silent Generation did.

Personal wealth is burning a hole in Boomer pockets and lighting a fire in their consciences, and they want to make sure it leaves a positive impact on the world. The psychological term for this is generativity; we know it commonly as legacy. The term generativity was coined by Erik Erikson in 1950 to denote “a concern for establishing and guiding the next generation.”

Looking at time volunteering as a donation, projecting $1 trillion in volunteer hours (read: free and needed labor for charities nonprofits), it’s a fact that “retirees volunteer less than other age groups [and] charities would be smart to figure out ways to increase their involvement, because once they do commit their time, they end up volunteering more total hours than any other age group, according to the report.”

Women lead the way in empathetic giving, following centuries old tropes of being more likely caregivers compared to men, as “retired women are more likely than retired men to contribute both money and volunteer time to charity, with 81 percent of retired women giving money compared with 71 percent of retired men and 29 percent of retired women volunteering versus 22 percent of men.”

According to Dr. Dychtwald, gerontologist and founder of Age Wave, “The rising up of this [philanthropic] demographic mass with more money and free time than we’ve ever seen is revolutionary […] It’s not just ‘where might we want to play golf’ but ‘how can we help people in need?’” He continues, “This is a big boon for philanthropy, but it’s not business as usual. “Boomers overwhelmingly want to make an impact on the world, and just writing a check doesn’t turn them on. They want to get back from their giving.”

For what seems like shortsighted advice, the New York Times published a piece called, Parents, the Children Will Be Fine. Spend their Inheritance Now. Without a hint of cynicism, falsely predicated on rosy outlooks and continued economic growth (a logic upon which there is no solid foundation), they claim that, the “parental instinct might seem loving and generous, but there is another way to look at it. All of this devotion to the next generation may also be the height of foolishness.” As in, making sure your offspring are in a better place after you die is foolish. They even go through the motions of citing Christopher Mayer, a Columbia Business School economist, who suggests reverse mortgages to allow parents to live lavish, without acknowledging the drawbacks or pitfalls, of which there are many, including negative amortization, reduced equity, heir transfer issues, and the newly acquired ongoing fees that drain newly acquired money through your reverse mortgage and passed on expenses.

The retirement (or lack thereof) of Boomers affects the job market in four major ways, according to The Balance. Workplace flexibility, first, as Boomers who still work require more flexibility and want less hours, though “only 48 percent of employers have made flexible policies that allow baby boomers to switch from full-time [sic] to part-time.” They fight for quality of life and fuel what Richard Florida called the creative class. Secondly, there are more job openings due to retirement, but, oddly, “there are fewer replacement workers to take over. This is causing what has been referred to as a ‘huge knowledge gap.’ Even if the economy is in a downturn, overall, there will still be a need for specialized workers to take over these new openings.”

A third way Boomers impact the job market is through not retiring. Because of increased government borrowing from “Social Security as well as the continuing rising costs of living, the unfortunate reality for many baby boomers is that full retirement is not financially viable.” And finally, pay spikes because, “in the labor market, and specifically in the technology job market, when there are jobs available and not enough workers [a problem of education shortfalls and draconian immigration policies], wages go up to attract and retain the necessary workers. A large group of baby boomer retirements is no exception. Most tech-related positions were expected to have some form of salary increase in 2016,” and we can only expect that to see that increase.

A test case: Retirement

I spoke with local retiree and just barely Silent Generation baby, Jim, at the Miner’s Tavern over a beer. Congenial and happy with his life, I was curious as to what went so well for him. A few things came out in the conversation: he retired with a strong pension from a public education system in California, realizing that his 75 percent of pay pension checks were actually bigger than his paychecks thanks to the extra taxes and social security not being taken out. But that wasn’t it. He was aware of the world around him, disinclined to chase things as much as to chase happiness, and he was smart about his timing.

Jim tells me that his wife worked at the start of their life, and continues to do so, a strong feminist move that presaged the need for dual income families. He tells me that he was lucky to retire and work as an emirutus professor, enjoying the dual income of pension and pay. In an especially well-timed and crucial moment, in 2006, Jim was able to sell his home for peak value and avoid the wipe out most families endured. He bought a house in Colorado, just before housing seriously spiked. And then his social security kicked in. He’s never been happier, more comfortable, or more ready for what comes next, he grins to tell me.

Giving away all his money? Well, he’s not rich, he’s quick to say, but he’s definitely well off. He’s taken the advice of a trusted financial advisor who has guided him for decades and will keep the money headed down the bloodline. That is, he’ll divide it up between his own sons and let them pass it down as they see fit. There’s no need, he tells me, to spread it around.

It would seem that Jim is that late age, Silent Generation test case that is the model of what American (and American retirement) should have been. Public union erosion, reduction in benefits – basically all the awful stuff we discussed earlier – means cases like Jim’s are no longer the norm. As the Silent Generation had, the Boomers will not have, nore will Generation X, nor will Millennials. Retirement planning changes. It evolves and, over the course of your retirement planning, bequeathment planning, and beyond, you need to be cognizant of and adaptable to the changes.

Professor Huang reminds us, “Retirement planning is more challenging and risky in America than ever before due to changes in what has been termed retirement’s three-legged stool, consisting of Social Security benefits, pension plans, and private savings instruments.” Planning for retirement takes cognitive thinking and applying what he terms cognitive economics.

“There are many ways in which people can mess up retirement,” Huang is clear, “including saving too little, investing non-optimally, claiming Social Security too early, and outliving their savings.” The process is unclear and made murkier still with purposeful obfuscation of logics through the use of jargon, complicated processes, and the preying upon by those who have ill intent. That nest egg is under constant threat. “The reasons things can go wrong are varied also, including finite cognition, information overload, and outright fraud. Because of this multiplicity of retirement problems and causes, no one magic bullet policy prescription can or will fix all the possible problems,” Huang says.

There is a path to retirement success, but it’s going to take serious work on your part. Huangy advocates in his article that “the American federal government help Americans improve their decision-making and thinking about retirement by educating Americans about and subsidizing: (1) thinking architecture, such as Shlomo Benartzi’s Goal Planning System process and Chip Heath and Dan Heath’s WRAP heuristics procedure, (2) thinking technologies, such as thinking apps, financial entertainment games, and serious games about decision-making, (3) thinking mindfully about how to become financially ready for, and what to do in, retirement, and (4) thinking more societally about retirement planning to change the social norm in America from individually responsible retirement planning to societally responsible retirement planning.”

Final word

Millennials have it bad for all the reasons mentioned (thanks, Mom and Dad). The future is terrifying for those of us brave enough to look ahead. This is not speculation, but is based on clear reviews of Silent Generation and Boomer statecraft over the last few decades, and where that has gotten us. Generation X are facing their last decades of meaningful work, meaning they’re getting laser focused on retirement saving given the fact that their current retirement savings are staggeringly low relative to need. Silent Generation bequeathments to Boomers and beyond, and subsequent inheritances from Boomers to GenX and Millennials in the next 30 years means the kids will (probably) be ok. For the most part.

It stands to reason, of course, that hundreds of millions of families are without the savings, future bequeathements, or even the moderately rosy outlooks due to numerous factors, including (most prominently) denied economic access based on race, gender, and ability, among other things.

Boomers will give their hearts in the form of checks and volunteray hours, as philanthropic giving and charity take precedence in late life. They could do worse. They’ll will go out with a bang, and quite a few (bequeathment) bucks, with the goal of leaving the world in a better place than they found it and arguably better than where they’ve taken it thus far.

Assuming that we can reverse the infinitely unreasonable tax burden congress passed and President Trump signed, the prospect of nuclear war with North Korea, and the end of life on the planet via climate change, the kids (GenX and Millennials) are going to be ok. It’s time to start and stay planning. There’s no time to play. Tomorrow will be here sooner than any of us think.

Irina Ratsek