Terri and I drive through winding roads, blurry patches of faded green and yellow pass beyond the window. We make small talk during our 25 minute drive. Terri is 67 and has been an Uber driver for for the last few months as a way to supplement her income.

“I like driving. It’s relaxing, I get to meet all kinds of different people and I get to choose my own hours. That’s important to me. I have to be able to pick up the grandkids from school.”

Terri retired a few years ago, just before she turned 65. A teacher and coach, she was enrolled in a pension plan, but as the years went on, she found she was struggling to afford all of things she had planned for retirement. So she went back to work (she also substitute teaches).

“I don’t necessarily have to work, but I figure I might as well work while I still can,” she said. “Besides I get bored – I’ve always been a busybody.”

This is a common predicament for those approaching retirement – going from a salary to a fixed income is difficult, and often Americans don’t have enough saved up to enjoy 20 years or more without working and, yes, lifespans are continuing to increase. Older people are staying in the workforce longer, by choice, by necessity, and sometimes by force as retirement ages increase – facing a reduction in retirement benefits, higher costs of living, and stagnant social welfare programs. It’s having a significant impact on our economy not only for those hoping to retire someday soon, but also for those just entering it.

CHANGING DEMOGRAPHICS

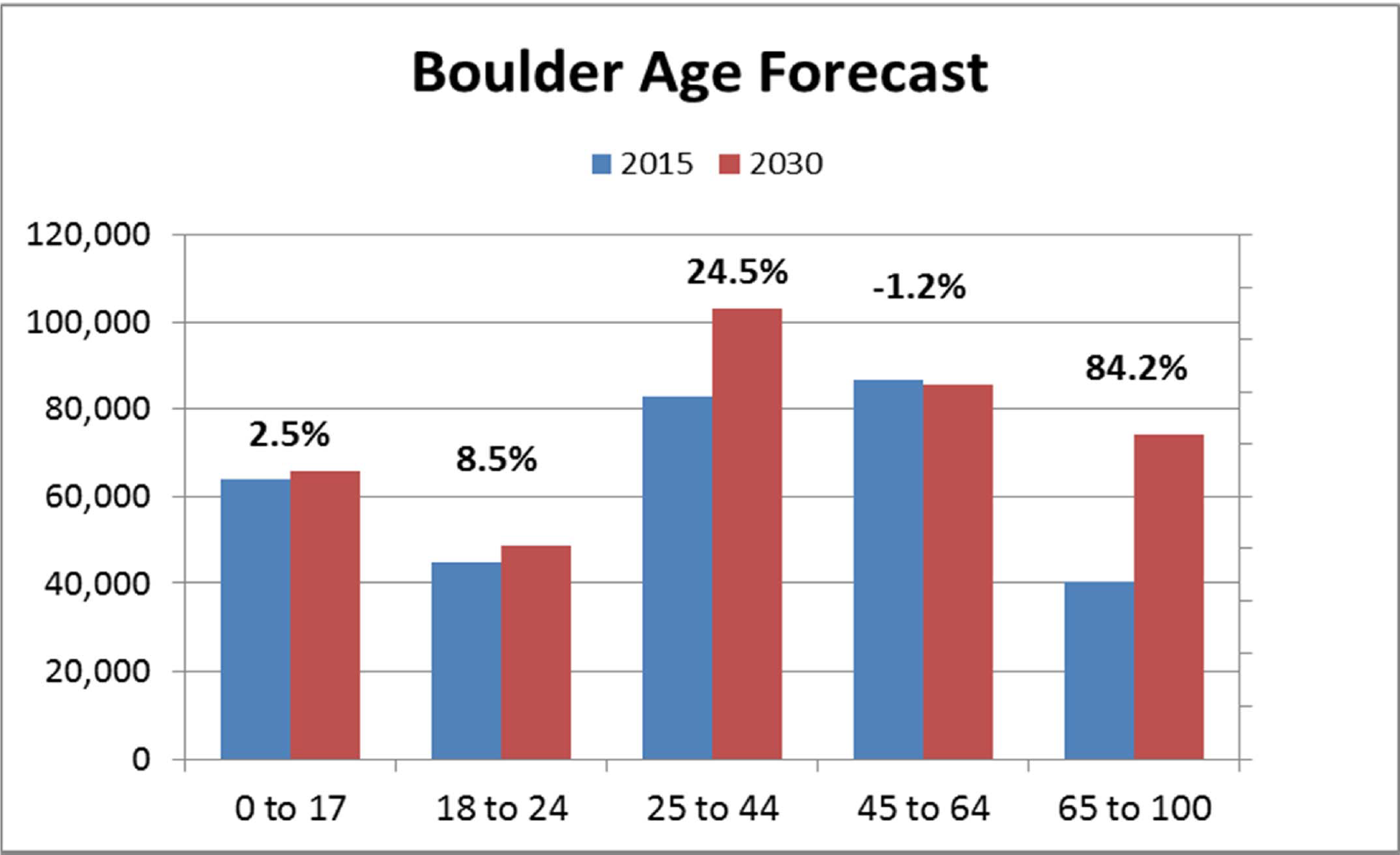

Our workforce is about to undergo a serious change of demographics with the over 65 population in Colorado increasing from around 800,000 to 1.2 million by 2030 (hint: that’s not far away at all). The share of older adults among Boulder County’s population is increasing as well: in 2010, adults aged 60 or older comprised 15 percent of the population; by 2035 that figure is expected to reach 26 percent and stabilize for at least 15 years, according to the Area Agency on Aging.

The shift in labor will mean changes for our economy, with younger workers outnumbering older ones for the first time in decades. Trends show that the retirement age has been increasing, so while seniors will gradually transition out of the workforce, it will have an immense impact on every sector of our our economy.

“It’s how they spend their dollars. There will be lots of growth in healthcare and food service,” says Elizabeth Gardner, Colorado State Demographer. “We laugh at it, but older people eat out. My mom is the perfect example, she eats at Panera three times a week.”

“What’s fascinating is it’s across the spectrum. There is almost no industry that isn’t impacted by aging spending – transportation, accounting, agriculture – but the biggest is [sic] hospitality and healthcare.”

With a larger percentage of our population over the age of 55, healthcare needs will rise dramatically, not only for hospitalizations and long-term care facilities, but also for doctors, specialists and nurses. Healthcare is already an in-demand field with a well-reported nursing shortage in Colorado that is expected to worsen as the 35 percent of nurses who are 55 or older age out of the workforce.

“You’ve got this large share of people aging, a lot are aging into groups with lower participation rates,” Gardner said. “At older ages people participate in the labor force at lower levels. They really start aging out in their 50s.”

As people age in the workforce, they become less productive, according to a study by the University of Paris-Sorbonne. They also participate less, which just means that a larger percentage of that population is not active in the workforce, either working part-time instead of full time, or not at all.

The peak labor participation rate is in 45 to 54 age group and then it drops off, according to the state demographer’s office. About 85 percent of 44 to 54 year olds are actually in the labor force; for 54 to 65 it drops to 75 percent of those in the workforce. Over the course of ten years participation in the labor force drops ten percent, and for those over 65, the drop in participation is even greater at 25 percent. Although that number seems drastic, it’s actually an increase. back in 1990 it was 15 percent.

“A lot of it is we are working more desk jobs. We’re healthier than we’ve been, and we’re not doing as much hard labor, if you go back decades that what they worked in,” Gardner says.

“We have a lot of accommodation with technology and all sorts of things that with age-limiting disabilities you have more of a chance to be working.”

Gardner says another reason people are staying in the workforce longer is the desire to continue working. We are living longer, so having 30 years of vacation isn’t necessary, for most people 15 is fine.

In Boulder county, 58 percent of older adults are fully retired, which is on par with state averages while nearly 40 percent of older adults are working full or part time jobs and 2 percent are seeking employment, according to the Area Agency on Aging.

The AAA’s recent study shows that the average age Boulder County adults plan to retire is 73, which is about three years lower than the average in Larimer County and equivalent with the state average; however Boulder County does have a higher proportion of older adults working in later life (75 and older) compared to the state average and Larimer County.

“My plan was to retire when I was 55. But I’ve always been an active member of my community and I realized… what was I going to do for the next 25 years? I knew I’d end up working anyway so I stayed with it well into my 60s,” Terri said. “I’m healthy and capable, and honestly, my benefits alone won’t pay the way.”

BENEFITS REDUCTION

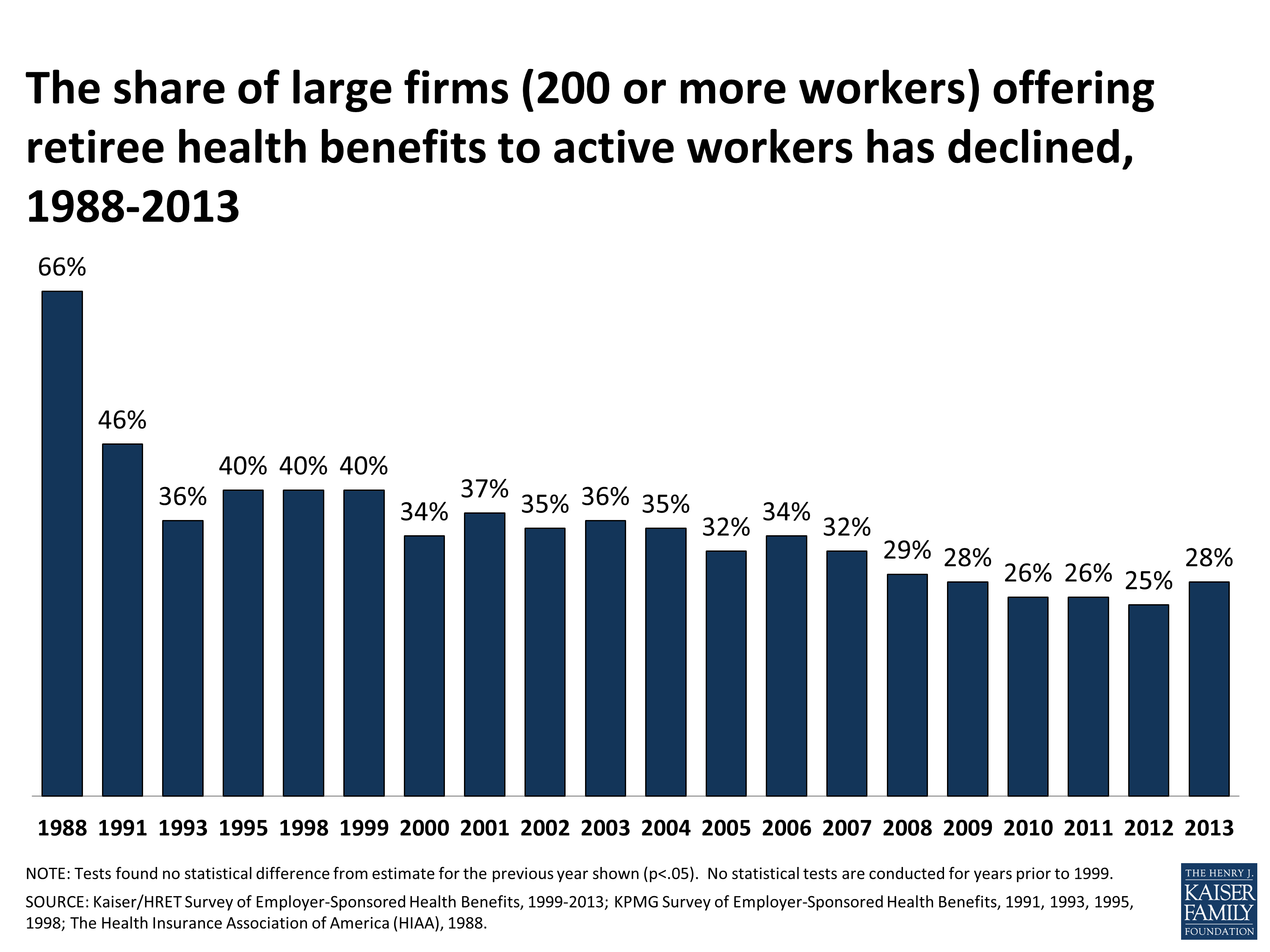

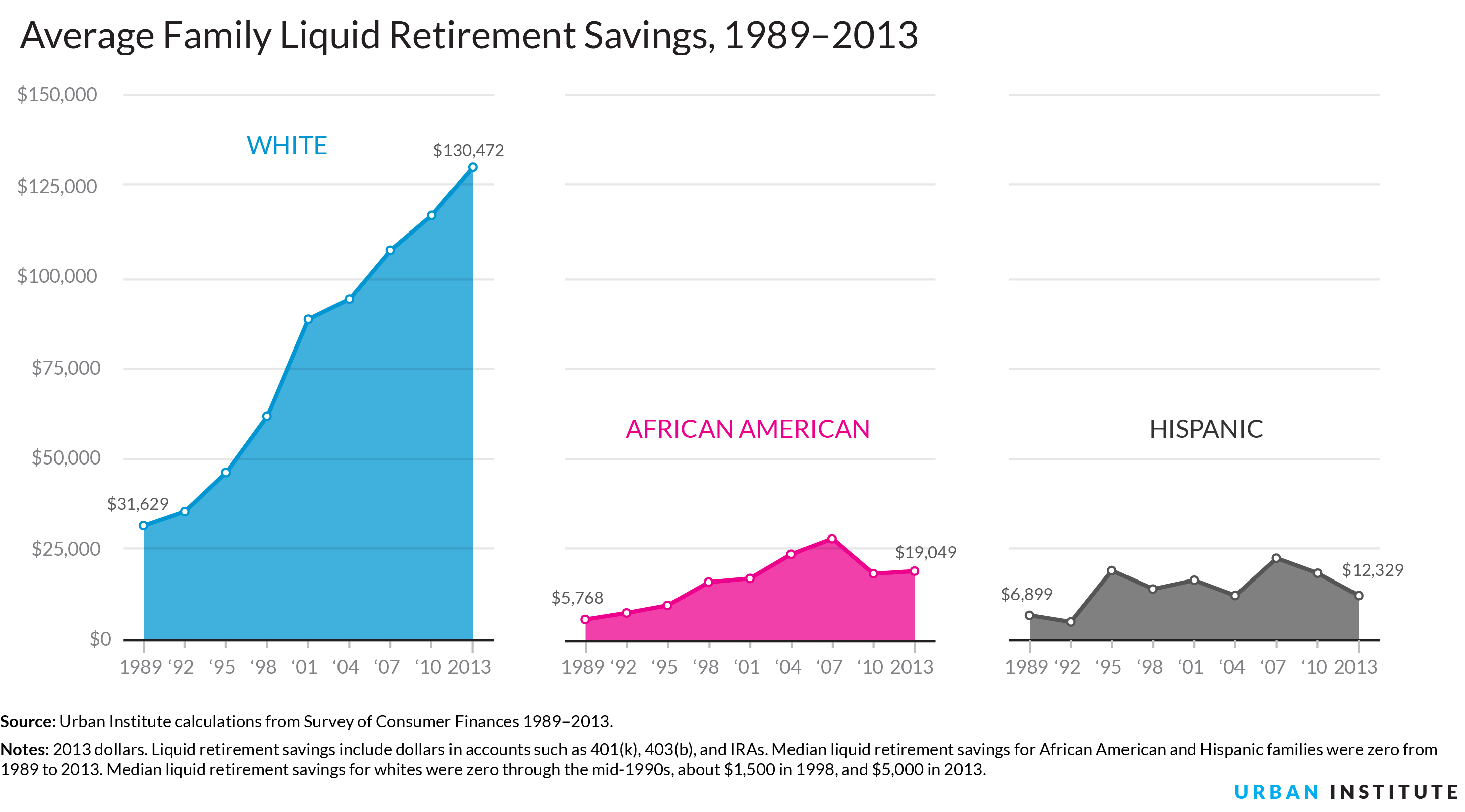

A lack of savings for retirement has also contributed to the number of older people staying in the workforce. Even worse, a recent study on American savings, reported by Fortune is gloom: “Thirty percent of younger boomers, those aged 54 to 63, have no emergency savings—more than any other generation…[and] only 29 percent of Americans have enough emergency savings to cover at least six months’ of expenses—a financial planning norm. This is down from 31 percent in 2017.” Over the last several decades both the public and private sector have made major reductions to employee benefits, which adds to the pain. Pensions have been more or less eliminated, replaced by 401k, IRA and other retirement savings accounts, which don’t always adequately help people save for retirement.

While some working public sector jobs still have pensions many have done away with them altogether or reduced them, which has contributed to the reduced productivity of the U.S. economy, according to the University of Paris-Sorbonne study. The decrease in pensions correlates to the rising gap between the rich and poor, said French economist Thomas Piketty at an economic conference in Paris.

From 1980 to 2015 the proportion of private wage and salary workers participating in a pension program fell from 38 to 15 percent, according to the U.S Bureau of Labor Statistics. And although many public sector jobs still offer pensions, of the 75 percent of state and local government employees, 57 percent participated in frozen defined pension plans, which are not open to new employees.

From 1980 to 2015 the proportion of private wage and salary workers participating in a pension program fell from 38 to 15 percent, according to the U.S Bureau of Labor Statistics. And although many public sector jobs still offer pensions, of the 75 percent of state and local government employees, 57 percent participated in frozen defined pension plans, which are not open to new employees.

In line with American corporate ideals, eliminating pensions means companies no longer have to attract workers with retirement benefits, which leaves them without the safety net of increased taxes to help fund pensions, as is the case with most European countries.

Note that European productivity and revenues parallel Americans, while European savings and quality of life are both regularly reported as much higher than their US counterparts.

What’s more common are 401k plans funded mostly by employee contributions, which eliminates the corporate need to fund a pension, which eats into a company’s bottom line. For the last 40 years we’ve been prioritizing corporate profitability over employee wellbeing and retirement, coinciding with the eradication of unions. Contribution plans have had a hand in the growing economic disparity. Higher paid jobs tend to offer better benefits and employees with higher salaries can contribute more either in percentage or dollars because their income allows more discretionary spending and investing.

About 43 percent of private workers contribute to their 401k or other contribution plan, leaving a majority of the population unprepared for retirement. The average 401k balance was $106,000 at the end of the third quarter of 2018, according to Fidelity investments, one of the leading contribution plan management firms. That number is an all-time high, but think about how far $100,000 will get you over the course of 30 years: that’s an average of only $3,333 per year. Eliminating mortgage payments or rent, that’s barely enough to pay your bills, let alone have any kind of purchasing power left over, even factoring in payments from social security and healthcare coverage under Medicare.

Those collecting social security, however, will see an increase in payments beginning in 2019. Recipients will see a 2.8 percent increase in their payments to ‘keep up with inflation,’ officials say. The 2.8 percent cost-of-living adjustment is the largest increase to social security since 2012, with the average benefit for a retired worker expected to climb by $39 to $1,461 per month. Married couples will see an estimated $67 increase to $2,448 per month beginning in January of 2019.

For younger workers who contribute to social security as part of their payroll taxes, that means you are likely to pay more, a frustrating idea considering the uncertain future of the program, which could potentially exhaust its trust funds around 2034 without intervention, especially as politicians work to defund social security while calling it an “entitlement” even though it is self funded. It is also frustrating considering wages have been growing at a slower pace than inflation for decades. The average yearly wage in 1970 was $6,186, which is the equivalent of making $41,399 in 2018, according to inflation calculations made by the U.S. Consumer Protection Index, well above current minimum wage salaries and most entry level jobs.

Lack of benefits, stagnant wages, and a healthcare system struggling to be funded – a health in homes service in Denver recently got de-funded – it’s no wonder older people are working longer and re-entering the workforce to make a few extra dollars; they can go a long way.

Portrait Of Female Owner Of Gift Store With Digital Tablet

LABOR CHALLENGES

Meet Debra. Debra left a successful career in banking to stay home with her children and get away from the stress of corporate America. She was almost 50 when she made the decision to leave, with the intention of re-entering the workforce once her children left for college in four or five years, which is when the recession hit.

“Finding work, especially in banking, during that time was a challenge,” she said. “I was too qualified or experienced, companies didn’t want to pay me at the higher salary. I ended up teaching business classes part time.”

Without the strain of the recession the job hunt is undoubtedly easier, but for those older adults it’s still a significant challenge. Older people tend to be unemployed for longer periods of time, up to 27 weeks, than their younger counterparts. Employers seem to discriminate against the long-term unemployed, which creates a perpetuating cycle of un- or under-employment. Being out of work for a substantial period of time can lead to longer periods of unemployment, according to AARP. So for those who have been out of the job market for months or years after retirement, re-entering the workforce can be an uphill battle.

In Boulder County, however, finding work in older age has gotten easier, says Jacob Bielecki with the Area Agency on Aging – 25 percent of those re-entering the workforce after retirement reported finding work to be a minor problem, not a mj. Boulder County is again below the state average with 23 percent of older adults reporting at least minor challenges building skills for paid or unpaid work.

Workforce Boulder County might have something to do with this. The free services help people of all ages, employed or unemployed, with resumes, trainings and more. Its workshop – Transition, Transform, Transcend – is geared specifically for those 50 or older.

“We want to address the fact that people over 50 statistically have a longer time being unemployed while looking for work. It usually comes as a shock,” says Deb Blankenship, with Workforce Boulder County. “You hear a lot of ‘I usually have no trouble getting work’ or ‘I’m not getting hired at interviews’ or getting the response that they are too qualified. They report a bit of agism, and statistically it bears out.”

A study by AARP shows approximately two-thirds of workers ages 45 to 74 have experienced or seen age discrimination in the workplace. The Colorado Equal Employment Opportunity Commission has seen a drop in the number of recent cases filed from 659 in 2009 to 515 in 2016, while, over the last eight years, the 25 percent of Boulder County older adults reporting any incidence of feeling like they have been treated unfairly or discriminated against hasn’t changed.

“I wouldn’t say I felt discriminated against, but I feel like my age definitely played a role in my job search,” Debra said. “I was asked about my commitment to the company, which as someone over 60, I don’t think I would have been asked that question if I was 45.”

Blankenship says that concerning yourself too much on age and the potential for discrimination can hurt older adults in their job search. “If you focus that you are over fifty and are worried about age discrimination and you are thinking about it, it’s going to telegraph to whoever is interviewing.”

The best way to combat potential discrimination, lack of confidence or changes in technology upon returning to the workforce is preparation. WBC offers resume help, intense training, interview help, networking, and LinkedIn workshops.

“A lot of people think Workforce is just for blue collar jobs; but the training reflects the population that lives here. Whether you have multiple advanced degrees, PhD, we all have a tough time getting a job,” Blankenship says. “I tell people: Millennials and older adults have a stigma around them and people believe a lot of that – check your assumptions and prejudices you don’t know you have; they might be getting in your own way.”

UP AND COMING WORKFORCE

Despite what the outlook may seem – bleak, ‘I’LL NEVER BE ABLE TO RETIRE!’ level depressing – having more older adults in the workforce isn’t necessarily a bad thing, though it’s not really a good thing either. The U.S. economy is undergoing structural changes that are largely attributed to the high percentage of our population growing older and transitioning into these ages with lower participation in the labor force, a report by the U.S. BLS says. With fewer people ‘in their prime’ working, the economy has limited capacity to generate as much economic output, even as annual growth in GDP is expected.

With a large percentage of our labor force set to retire, the labor force is expected to grow at a glacial annual rate of 0.6 percent, largely do to the slow expected population growth of those 16 and under, according to the Census Bureau.

“Our labor force at the young end is completely falling off,” Gardner says. There has been a massive decline in birth rates since 2007, so as much as the Colorado born and raised might dislike transplants, we’re going to need a lot more of them to make our economy viable.

As older workers retire, there’s even a chance that younger workers, who have been stifled by stagnant wages, will see their earnings increase. Currently, workers over the age of 65 saw their monthly earnings increase 80 percent between 1994 and 2015 when adjusted for inflation compared to 32 percent for workers between ages 35 and 54.

It also means we will have to get more creative in our workforce, beyond automation and technological advances. In certain industries that will be particularly in demand, like healthcare, that means things like telemedicine and other technologies that can more efficiently and effectively deliver services.

“We are seeing a lot of automation, because we actually need it. It will take a few jobs but those at the grocery job checking people out, we can’t have enough of them, can’t find enough fast food workers; if you can automate components it will actually be beneficial,” Gardner says. “And I think you will see more and more of that movement of people leaving and those moving up and in.”

The labor force is very tight right now, which means many people are stagnant, or moving from job to job and we’re going to continue to struggle with that over the next ten years. But ultimately the more people we have participating in our economy, the better off we all are.

“If you are making and spending money, you are also creating jobs,” Gardner says. “We have a bigger economic impact – you create more jobs having more people working than not.”

Retirement savings and benefits are decreasing. Cost of living is rising. Wages are stagnant or growing slowly. Older people staying in the workforce longer is projected to be a continual trend, not just a generational one. The concerns over Millennials’ financial health are justified – they began entering the workforce during a recession and have tremendous debt tied up in student loans, and it will likely mean that they will be staying in the workforce even longer than their Boomer parents.

It’s likely not going to end with Millennials, younger generations, and even Gen Xers, won’t receive full Social Security benefits until they are 67, five years beyond the age Boomers can begin seeing those benefits. Based on data then, our workforce will continue to be less productive, citizens will struggle to afford retirement, meaning our workforce and social programs have a higher potential to be overextended. Addressing these problems before they balloon will require legislative and corporate responsibility. Doesn’t leave us with much hope, does it.